Tax News

Important 2024 Tax Dates

January 16: 4th quarter estimated tax payment for 2023 due.

January 31: W2s and 1099s due to employees/contractors.

February 15: Brokerage and financial documents due to account holders.

March 15: Calendar year partnership and S corporation returns due.

April 15: Individual and C corporation tax returns due.

April 15: 1st quarter estimated taxes due.

June 17: 2nd quarter estimated taxes due.

September 16: 3rd quarter estimated taxes due

October 15: Individual returns on extension due.

January 15, 2025: 4th quarter estimated taxes for 2024 due.

Important Tax Changes

For 2023 tax filing, the majority of tax changes are associated with EVs and home energy improvements as found in the Inflation Reduction Act, as well as changes to IRAs and 401Ks as found in the Secure 2.0 Act. Details below.

The 2023 Social Security wage cap (maximum wages taxed for SS) will be $160,200, an unprecedented 9% increase from 2022. The 2024 cap will rise to $168,600, a significant increase of 5.2%.

In an unpromoted legislative action (surprise!), California removed the wage cap for SDI tax. Similar to Social Security, SDI tax has been applied to a maximum of wages ($153,164 in 2023 taxed at .9%). Beginning in 2024, all California wages will be subject to a 1.1% SDI tax, and with the TCJA SALT limitations in place through 2025, this increased SDI tax will remain non-deductible for most Schedule A itemizers.

Tax Rates, Income and Deductions

Standard deductions for 2023 are $13,850 for single filers, $27,700 married filers, and $20,800 for head of household filers. In 2024 these increase to $14,600 single, $29,200 married, and $21,900 for head of households. 65+ 2023 add-on deduction is $1,850 single, $1,500 joint increasing to $1,950 and $1,550 respectively.

The Inflation Reduction Act instituted a new 15% minimum tax on corporations, but individuals were spared changes to the tax brackets. There remain 7 - 10%, 12%, 22%, 24%, 32%, 35% and 37%. Per 2018 TCJA the bracket dollar amounts are adjusted for inflation and will increase approximately 5.4%. You can see the brackets here. California standard deduction and tax rates can be seen here.

Maximum individual pre-tax FSA/HSA contribution for medical expenses rises from $3,050 for 2023 to $3,200 for 2024 with $6,400 maximum per family. The Schedule A deduction for medical expenses AGI threshold remains at 7.5% for those itemizing.

Unremimbursed employee expenses, legal fees, investment advisor fees and other miscellaneous itemized expenses remain non-deductible on the Federal return through 12/31/2025 when the 2017 TCJA changes expire. Since California did not conform, we keep an eye on these potential deductions for State purposes.

Energy Credits

Beginning in 2023 the maximum electric vehicle credit increased back to $7,500 but with some provisions relating to minimum amounts of US sourced components for a vehicle to be eligible (emphasis on batteries). The vehicles must also be assembled in the US to qualify. EVs that do not meet these requirements are subject to the previous maximums and phase-outs. So this is all a bit murky at the moment as most EVs do not qualify for the increased credit (Consumer Reports has a list of EVs that currently qualify or may qualify). There are new price and income restrictions as well: Passenger vehicles must sell for under $55,000 and SUVs, vans and trucks for under $80,000. MFJ taxpayer income must be less than $300,000 ($150,000 single). Furthermore, there is a new option whereby the car buyer can reassign the credit to the dealer as part of the vehicle downpayment, if they can attest to qualifying under the income limits. For higher earners leasing an EV may prove a better option as the dealer is eligible for the credit and may pass it on in some fashion to lower the lease payment.

The new credit for buyers of used EVs is more straight forward. The credit is 30% of the purchase price (up to $4,000) for EVs that are older than 2 years, bought from a dealer (private party sales ineligible), and that it is the first resale of the vehicle. The vehicle must be sold for less than $25,000. The income limits for the used EV credit are stricter: $150,000 for MFJ and $75,000 for Single filers. This credit also began in 2023.

The 30% credit for EV charging stations was restored and extended through 2032.

Beginning in 2023 the residential energy credits for insulation, windows, doors, and furnaces change significantly with the $500 lifetime credit cap being replaced with an annual $1,200-$2,000 credit. This credit is in place through 2033. 2024 sees a new rebate program funded by Washington, administered by the states, for the above energy efficiencies as well as for various appliances. The rebate list is extensive and too detailed to include here but the information is available online. Note: Anyone can take advantage of the energy tax credits, but the rebate program is to be means tested, so higher earners will not be eligible (exact details are not clear at this time).

The solar energy panel and battery storage tax credit is raised back up to 30% of the cost of panels and batteries, including labor for installation. This credit is also extended through 2032.

Children & Dependents

The maximum pre-tax dependent care FSA contribution for 2023 is $5,000. Child & Dependent Care Expenses (Form 2441) is $3,000 for one child and $6,000 for two or more children. These are the expenses paid for pre-K childcare, Kindergarten, or after-school and summer activities for children until their 13th birthday. 2024 should see no change.

The Child Tax Credit for 2023 is $2,000 per child up to age 16 and $500 per older dependent (phased-out for higher earners). Again no change is expected for 2024.

Up to $5,000 may be withdrawn from a retirement plan without penalty for up to one year after birth or adoption of a child.

You may now withdraw up to $10,000 from a 529 plan during your lifetime to repay student loans of an account beneficiary (or their siblings) without tax or penalty. Additionally, a 529 may now be used tax-free to pay for an approved apprenticeship program. Starting in 2024 up to $35,000 in 529 funds remaining after 15 years from account formation can be rolled over to a Roth IRA; this is capped annually at the current contribution limit (e.g. $7,500 max each year). This is a fantastic opportunity for tax-free growth using surplus college savings with one caveat -- California does not conform; the earnings portion calculated in the roll over is taxed and also subject to a 2.5% penalty.

Retirement/Estate Planning

Beginning in 2020 the starting age for required minimum IRA distributions was raised to 72. This again changes significantly in 2024, see Secure 2.0 Act below.

The Social Security cost of living increase for 2024 will be 3.2%.

Maximum Qualified Charitable Distributions (direct transfers from an IRA to a charity) remains at $100,000 for 2023 and increases to $105,000 in 2024 and will adjust for inflation onwards. You must be 70-1/2 years or older to make this distribution.

IRAs inherited from people other than your spouse must now be distributed within 10 years of death. This does not affect IRAs inherited before 2020.

Stipends and fellowships are now considered income for IRA contributions.

Max 2023 401K salary deferral is $22,500 ($30,000 age 50+). In 2024 max 401K contributions increase to $23,000 ($30,500 age 50+). Regular IRA contributions for 2023 rise to $6,500 and rise again to $7,000 for 2024 with the additional $1,000 "catch-up" for those 50+ unchanged from prior years.

Gift tax exclusion rises in 2023 to $17,000 per donee to any single individual and will increase again in 2024 to $18,000.

The 2023 $12.9 million base unified credit exclusion amount for estate taxes increases to $13.6 million in 2024.

Secure 2.0 Act

This legislation modified significant aspects of retirement funding and distributions, many not coming online until 2025 or 2026. Below are some of the major changes in effect at this time:

Required mimimum distributions now begin at age 73 for those born in 1951 through 1958 and age 75 for those born after 1958. RMDs will no longer be required from Roth 401Ks.

Business owners/self-employed individuals can now establish Roth-SEP IRAs. Like all Roths, these accounts are funded with after-tax dollars.

Earnings distributed in association with correcting excess contributions to IRA plans will still be taxed as before, but will not be subject to the 10% early withdrawal penalty.

The list of exceptions to the 10% early withdrawal penalty on retirement distributions has nearly doubled, including an allowance for a $1,000 withdrawal for "personal emergencies" that requires no third party certification.

Business & Self Employed

Business meals with clients and during travel return to the pre-COVID rules at 50% deductible. "Entertainment" expenses remain non-deductible through 2025.

The 2023 standard business mile deduction rate is 65.5 cents and rises in 2024 to 67 cents.

Maximum 2023 401K/SoloK/Roth 401K salary deferral is $22,500 (with an additional $7,500 catch-up allowed for ages 50+). In 2024 max 401K etc. contributions increase to $23,000 ($30,500 age 50+). Maximum 2023 SEP contribution is $66,000 and increases to $69,000 for 2024. Remember SEP and SoloK contributions depend on net self employment income; I advise holding off on contributions until your tax return is complete to avoid possible over-funding. Contributions can be made for the preceeding calendar year through the filing due date, and in the case of SEPs, up through the October extended filing due date.

Remember, if a business does not offer a retirement plan to its employees, it must be registered with the mandatory CalSavers program to avoid possible penalties. Businesses with no employees (other than a single owner) are exempt from CalSavers.

Beneficial Ownership Reporting For Businesses

New for 2024! From the organization who brought you the FBAR: FinCEN launches another intrusive and annoying reporting requirement!

All businesses formed in 2024 must report information on their "beneficial owners" to the Federal government within 90 days of formation. Businesses formed in 2025 and going forward will have 30 days from formation to report. I already have a business, you say? You have until 12/31/2024 to report. Filing will be done online through the FinCEN website, and once a business has intially filed, it only files again if there are changes to any owner information.

Which businesses are required to report? The simplest(?) summary: Any business entity “created by filing a document with a secretary of state or similar office under the law of a state.” Basically, if you formed a business entity by filing with the California Secretary of State office (or similar office in another state) you likely need to report – we’re talking Corporations/S-Corps, LLCs and LPs. Sole proprietorships, general partnerships, and non-profits will not report. Businesses with 20+ employees and $5 million+ in annual receipts are also exempt from reporting.

What information is being reported? Personal information on individuals with a 25%+ ownership interest in the business. Information is also required regarding senior officers (CEO, CFO, COO), and individuals with "substantial controlling authority" (e.g. board members).

Like the FBAR this new reporting provision is aimed at thwarting money-laundering and dodging taxes, etc. but its going to be a quite burden on a lot of businesses. Penalties for non-reporting are $500 per day with no maximum! The government is obviously taking this seriously.

If you have a business that seems to fall into the above discussion, or will be forming one, or are not sure -- we need to talk.

Cashless Transactions

The new requirement for apps/services such as Venmo, PayPal, Cash, Apple Pay, eBay etc. to issue 1099Ks was suspended for 2023, and will take effect in tax year 2024 with a $5,000 or 250 transaction reporting threshold.

IRS Identity Protection

The IRS is encouraging taxpayers to apply for a PIN to reduce risk of identity theft and prevent anyone from filing a fradulent tax return under your name/SSN. The easiest way to apply is to use this IRS link. A new PIN is needed each calendar year and is good only for returns filed in that year (i.e. cannot get one mid-year for next year's filing). So if you are interested, my recommendation is to get your PIN in mid-January. You have to set-up an IRS online account and verify your identity first; this can be done at any time. You only need to sign up once; your annual PIN will be assigned automatically (you will need to log in to your account to retrieve it). And of course I need your PIN to enter for efiling! More information available on IRS Publication 5367.

Cryptocurrencies -- The IRS' Latest Obsession

Over the last couple years, the IRS has ramped up its enforcement of compliance with crypto/virtual/digital currencies (Bitcoin, Dogecoin, Litecoin, Ethereum, Dash, etc etc etc). The IRS (again surprise!) believes most taxpayers who own these currencies fail to report their taxable transactions. Beginning with the 2020 tax return, all taxpayers were required to affirmatively declare if they had engaged in any virtual currency transactions during the year. Intentionally failing to report taxable income can have severe consequences. Be sure to provide us with all information concerning your digital currency transactions during the year.

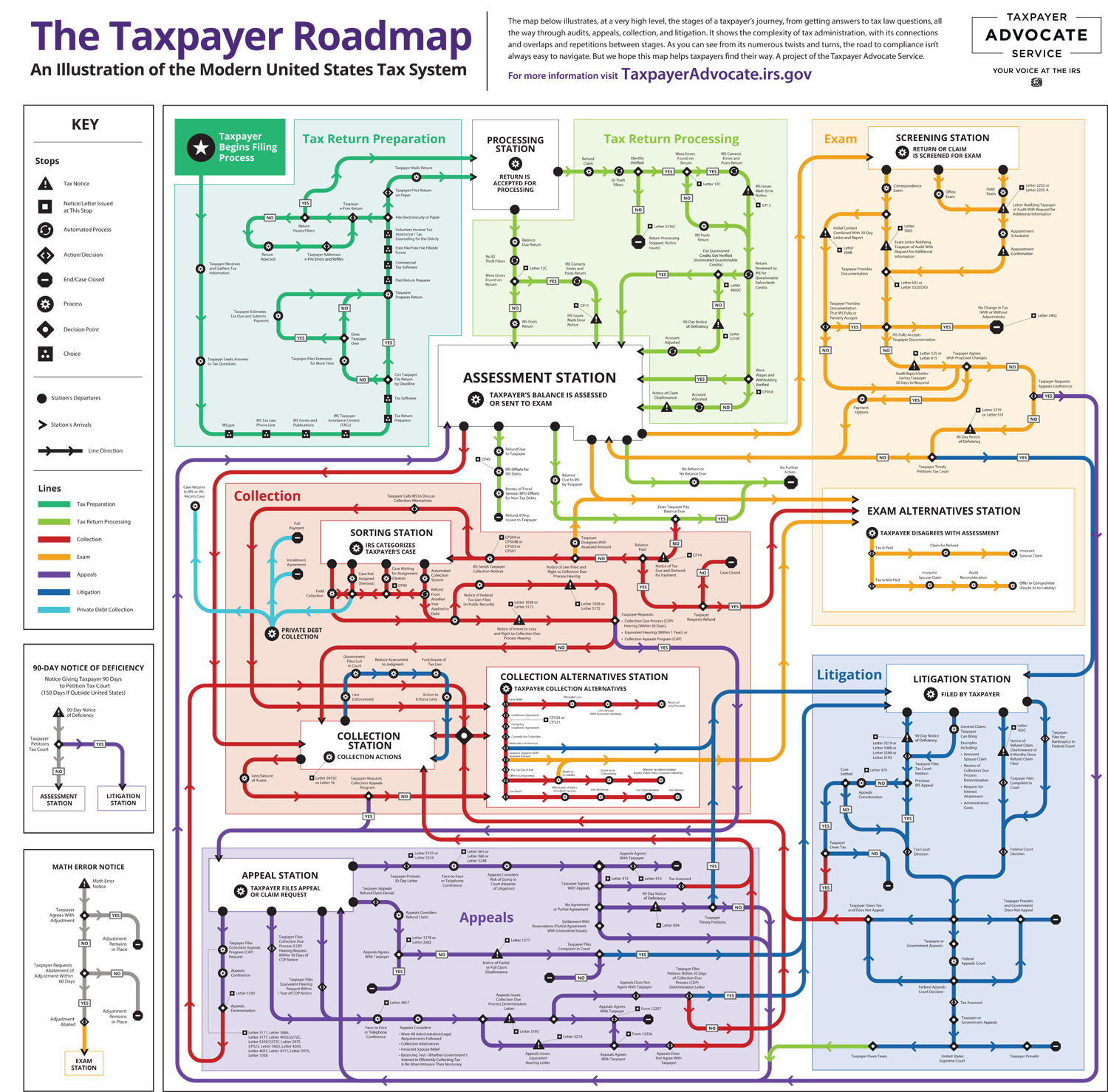

Your Annual Tax Journey

As the "road map" below highlights, preparing a tax return is just the first step in what can be a long process once it hits the IRS.

Who Pays Income Taxes Anyway?

The top 25% of all taxpayer earners paid 88.8% of all income taxes collected in 2020; they also earned 70.7% of all the reported money

(to be in top 25% your 2020 adjusted gross income exceeded $85,853)

The top 10% of all taxpayers paid 73.7% of all income taxes collected

($152,321 puts you in the top 10)

The top 5% of all taxpayers paid 62.7% of all income taxes collected

(top 5% means rich, right? Well, $220,521 put you in such rarified air)

The top 1% of all taxpayers paid 42.3% of all income taxes

(the oft maligned 1%ers, with income of $548,336+ are obviously doing okay)

Taxpayers reporting AGI under $85,853 in 2020 paid 11.2% of all income taxes collected, and those reporting under $42,184 (nearly half of all tax returns filed) paid 2.3%

(taxfoundation.org) latest IRS compiled data is from 2020

So, who pays the fairest share?

California Here I Come ... or go?

There's a lot of talk of the exodus from our increasingly crowded, expensive, drought-ridden, charred, sky-high taxes of a State. But does the data bear that out? Or is the ingress of the young and tech-savvy, Hollywood-hopefuls, and sun seekers of the California Dreamin' life holding steady?

According to the annual data study by United Van Lines and U-Haul, California is #9 on the list of outbound migration for 2022 with a net population loss of .3% (California was #3 in 2021). A glance at the map below indicates many outbound Californians are likely trekking to Idaho (#2 inbound), Texas (#4) and Montana (#6). In the East and Midwest #1 outbound New York and #2 Illinois residents seem attracted to South Carolina (#3 inbound) and Delaware (#7), with #1 Florida likely being high on the list of all interstate movers. California has seen a further net loss in population for 2023 as well, based on mid-year numbers; we can expect the 2023 version of the map below to show the Golden State moving back up the rankings for outbound migration.

Obviously, taxes play only a part of why people move, but there is no denying a strong correlation between low-tax, low-cost states and their population growth compared to high-tax, high-cost states.

Donating to Charity on the California Tax Return

If you look at Page 4 of the California Form 540, the entire page is dedicated to a list of approved charities you can donate to via the tax return. Donations made will reduce your overpayment/refund and the Franchise Tax Board will remit the donation to the Fund immediately. It is quick and easy and, if you itemize, tax deductible on your next year's Federal and California return (i.e. contributions made on your 2023 tax return filed in 2024 are deductible on your 2024 tax return filed in 2025). Keep in mind the donation is irreversible; it cannot be revoked or amended once the return is filed, even if later changes to the return are made.

Here is a list of the Form 540 charities and the amounts donated to them for tax year 2022 through taxpayer returns:

Alzheimers Disease Fund – $598,000

Breast Cancer Research Fund – $436,000

Cancer Research Fund – $437,000

California Neighborhood Tree Fund - $117,000

California Firefighters Memorial Fund – $227,000

California Peace Officers Memorial Fund – $137,000

California Sea Otter Fund – $322,000

California Senior Advocacy Fund – $121,000

Emergency Food for Families Fund – $620,000

Keep Arts in School Fund – $263,000

Mental Health Crisis Fund - $354,000

Native Wildlife Rehabilitation Fund – $350,000

Protect Our Coasts and Oceans – $352,000

Prevention of Animal Homelessness and Cruelty Fund – $308,000

Rape Kit Backlog Fund – $436,000

Rare and Endangered Species Fund – $479,000

School Supplies for Homeless Children Fund – $657,000

State Parks Protection Fund – $614,000

Suicide Prevention Fund – $268,000

Who's Preparing Your Taxes?

Do you realize that in 47 states there is no oversight, minimum or continuing education standards, nor any proof of competency required of anyone charging to prepare tax returns (the "paid preparer"). My prior hair stylist had to demonstrate more competency in order to be licensed than tax preparers in most states, and her mistakes grew back!

Of course, for those of you who engage the services of an enrolled agent, this has never been an issue. EAs have already passed an extremely comprehensive three part examination on the tax code and regulations, ethics, tax calculations and application for individuals, businesses and any other entity with a filing requirement. Furthermore, we must complete no less than 72 hours of ongoing education every three years (90 hours for NAEA/CSEA members). The IRS recognizes "Enrolled Agent" as the only designation with proven expertise in ALL areas of taxation.

Fighting An IRS Audit: You're On The Clock

There's nothing worse than seeing a letter in the mail box from the IRS. Actually there is something worse — doing nothing. One very important thing you should be aware of: When the IRS sends out a notice to you, the clock is ticking. Failure to respond escalates matters and, eventually, it's like not showing up in court ... BAM! Guilty! You have rights to dispute IRS claims, but they must be used within very specific timeframe's. Here's a LINK to an old but great article discussing the IRS timeline for its notices and collections processes (none of this has really changed in the last decade). Remember: Anything from the IRS in the mailbox means call your enrolled agent today.